Getting a Clear View of Revenues at Seasonal Businesses

Small business lenders are constantly searching for the right balance between gathering critical information from loan applicants and streamlining the application process. Lenders want to see the historical financials of a business, but as more financial information is requested, more applicants will drop out of the process.

When underwriting seasonal businesses, this challenge becomes even more acute. Most lenders, especially alternative lenders, ask for three months of bank statements. But with only three months of history, it’s impossible to understand the full impacts of seasonality on a business.

The result? Lenders face a high level of uncertainty and risk when underwriting these kinds of businesses.

To better offset this added risk, many lenders are looking to alternative data to supplement 3-month bank statements from applicants. The right alternative data can help by providing a more accurate view of annual revenue and highlighting any seasonality in a business’s revenues.

What are the risks of using 3-month bank statements?

One problem with using 3-month bank statements is that they can be highly misleading for businesses with seasonal shifts in revenue.

Most lenders rely on annual revenues, so they end up multiplying the revenues present in 3-month bank statements by 4 to estimate a business’s annual revenue. This projection is subject to seasonality, which means a lender can severely over or underestimate the business’s revenue.

Why do lenders request 3-month bank statements?

So why have 3-month bank statements become the norm for many lending decisions? Lenders face a trade-off: if they ask for more data at the time of onboarding, they can make better lending decisions… but friction increases, resulting in fewer applications. The less data that’s requested at the time of onboarding, the better the applicant experience.

Lenders have found that asking for 3-month bank statements versus longer-term bank statements significantly increases the size of their application funnel. Additionally, some ISOs (Independent Service Organizations) provide 3-month bank statements by default as part of a data packet on each small business lead, while other ISOs tend to guide lenders to use 3-month bank statements to increase the funnel.

What are the costs of underestimated or overestimated business revenues?

If applicant revenues are underestimated, SMB lenders miss out when they either decline healthy businesses that would have been able to make payments, or offer low loan sizes or lines of credit.

On the other hand, when revenues are overestimated, lenders end up taking on losses, approving businesses that may not be able to make payments, or providing loans or lines of credit that are too large for the business to repay.

Fireworks and tax accountants: real-world examples

To illustrate this problem, let’s consider three real seasonal businesses taken from Enigma’s database, which includes the current and historical revenues of more than 16 million businesses.

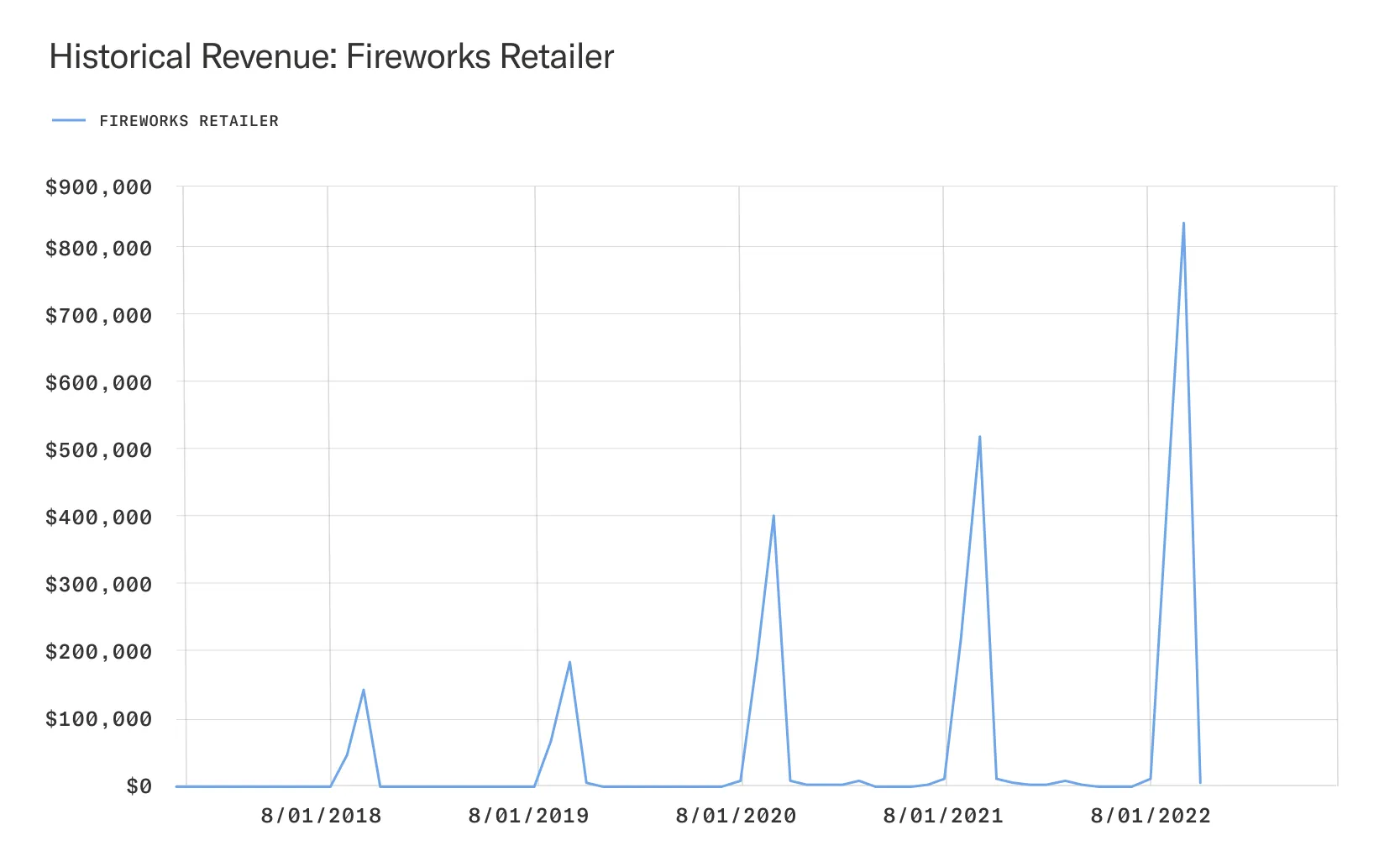

Our first example is a fireworks retailer that mainly sees revenue around the 4th of July every year. If this business applies in the winter months, it will look as though it has no revenue. As a result, its application will be declined despite sizable and growing annual revenue.

On the other hand, if this business had applied right after July, its annual revenue would be severely over-estimated, and the credit line or loan size given would also be overestimated and risky.

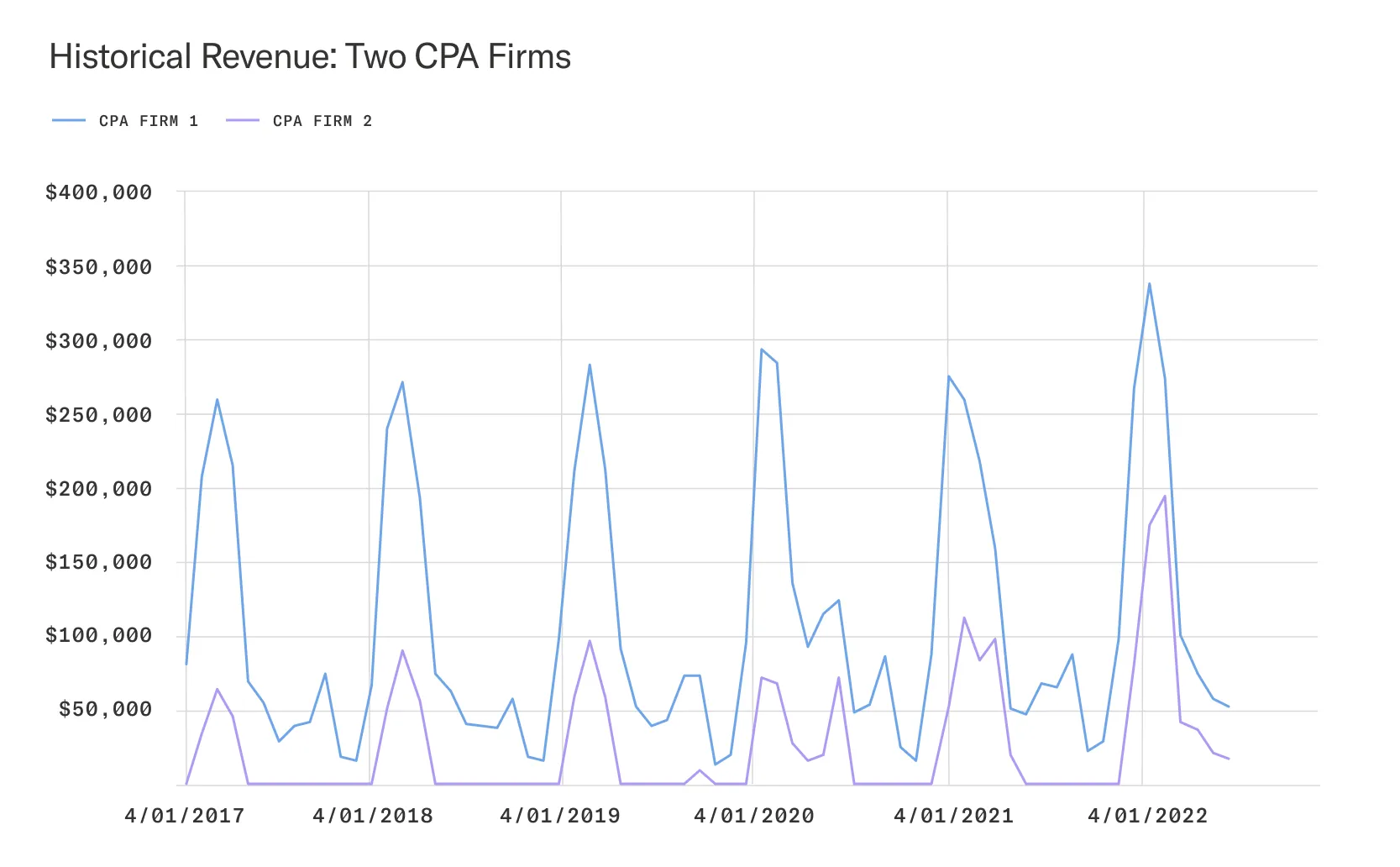

Similarly, accounting (CPA) firms primarily see revenue spikes during tax season. Below is a graph of two CPA firms. If either of these businesses apply in the fall, they will appear as having very low or no revenue, and their applications will be declined or handed low credit lines. If they apply right after tax season, their annual revenues will be severely overestimated, and the credit line offered may be too large.

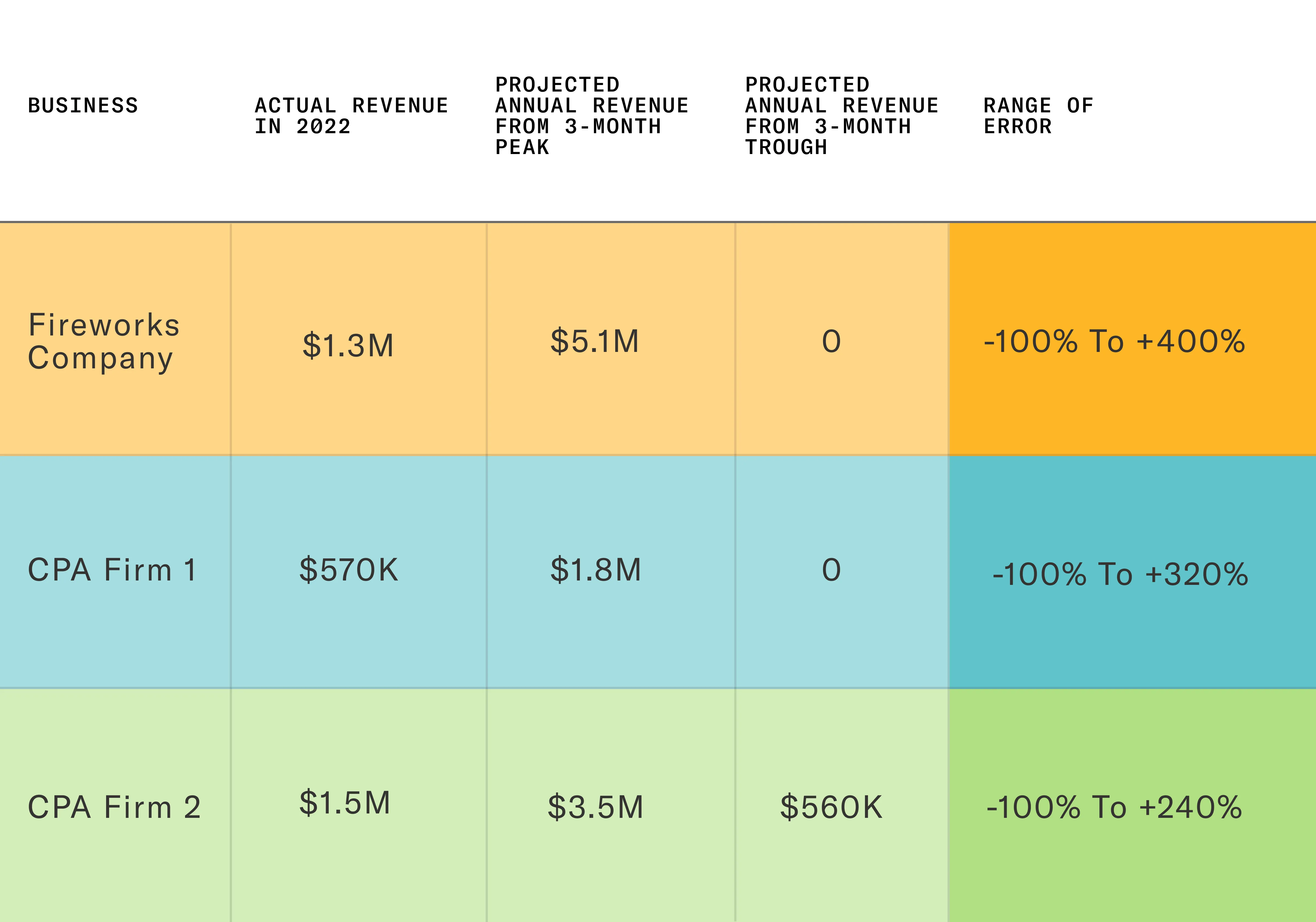

As you can see in the below table, the range of error for a lender relying on 3-month statements to underwrite any of the above three businesses would have a range of error of -100% all the way up to +400%.

How to supplement 3-month bank statements to de-risk lending (while protecting your funnel)

One solution to this problem is using alternative data to augment the view of a business’s revenues. Alternative data can help de-risk the usage of 3-month bank statements by providing a more accurate view of annual revenue. It can also help lenders better understand the seasonality of a business’s revenues.

At Enigma, we provide the full history of card transactions at a business going back to January 2017. This means lenders can get a clear view of seasonality and identify highly seasonal businesses based on past trends. Enigma’s data also enables lenders to project more accurate, seasonally-adjusted annual revenues from the 3-month bank statements they receive from applicants. Instead of just multiplying those statements by 4, lenders are now able to apply the appropriate projection based on historical revenues and seasonality trends.

Enigma’s data is pre-permissioned, which means there is no need to request permissions and create friction for applicants. It also eliminates the need for stipulations that reduce the acceptance rates of loans.

This results in the ability to safely underwrite more healthy businesses, reduce risk by identifying businesses that aren’t a fit, and reject businesses that aren’t a fit earlier in the funnel, saving costs.

Interested in learning more or getting a sample of Enigma’s data? Get in touch.