Sole Proprietorships, Micro-Businesses, and KYB: Why Traditional Verification Fails 82% of U.S. Businesses

According to the U.S. Small Business Administration, 81.9% of businesses in America operate without employees—and the vast majority of these are sole proprietorships. While this term might not be what we use daily to describe your local coffee roaster, freelance designers, rideshare drivers, or the countless other micro-businesses informally owned by a single person, this humble structure forms the backbone of American entrepreneurship.

By definition, a sole proprietorship is an unincorporated business owned and operated by one person. Unlike registered corporations or LLCs, most states require no formation documents. The business exists as the legal extension of its owner—a feature that makes perfect sense for entrepreneurs asking, “Why bother filing paperwork for Corporate Personhood when I’m already a Real Person?”

Sidenote: While sole props might not register with Secretaries of State, paperwork often does exist for micro-businesses. In particular, local regulations may require a microbusiness to register a Fictitious Business Name (FBN) or the name they Do Business As (DBA) with state or municipal authorities.

This simplicity that makes sole proprietorships attractive to entrepreneurs creates a verification nightmare for financial institutions. Millions of these businesses operate with real economic impact: they file taxes generating over $1.3 trillion in annual receipts, open business bank accounts, and employ contractors. Yet unlike their incorporated counterparts, they often lack the paper trail that modern KYB systems depend on. This puts fintechs and banks in an impossible position—choosing between regulatory compliance, fraud prevention, and business opportunity.

Why Sole Proprietorships Are Hard to Verify

At a structural level, sole proprietorships defy the typical inputs of most KYB checks.

- EIN (Employer Tax ID Number): While a sole prop can register an EIN, many don’t have one; instead they may file taxes under the owner’s SSN

- Business registration records: Typically don’t exist at all

- Business name (DBA): Fictitious Business Name (FBN) may not be filed even though their DBA is used in practice

- Legal Documents: No articles of incorporation or other organization docs

- Business Address: Often is a mixed-use address like a home office or can be inconsistent between records

The Hidden Cost of “Just Skip Them”

When faced with these verification challenges, three tempting but flawed strategies often emerge:

“Just reject them all” – This approach would mean turning away three-quarters of American businesses, including established operations generating hundreds of thousands in annual revenue. For payment processors and financial services companies, this isn’t just leaving money on the table—it’s abandoning the entire market.

“Default to manual review” – With sole proprietorships representing the majority of applications, manual review quickly becomes unsustainable. After a micro-business misses verification on a KYB check, processes either attempt to fall back to running a second, more costly KYC check, or skip directly to manual review, costing $20-50 per case and processing times of 24-48 hours. The economics simply don’t work for businesses expecting instant onboarding and customers who demand it.

“Lower the verification bar” – Perhaps most dangerous, loosening standards for sole props creates an exploitable gap in your defenses. Sophisticated fraudsters understand these systemic weaknesses and actively target institutions with inconsistent verification standards.

The reality is that regulators don’t care about your business structure when enforcing BSA/AML requirements. A sole proprietorship laundering money or facilitating fraud creates the same regulatory risk as any corporation—but traditional KYB tools leave you blind to 73% of the market.

What That Means for Risk and Compliance Teams

- False negatives: Rejecting real, successful businesses that don’t meet formal requirements

- Manual review bottlenecks: Time-consuming escalations to sort out ambiguous profiles

- Missed fraud risk: Approving bad actors who leverage the ambiguity of sole proprietorships to bypass common screens

Verifying Sole Props with Confidence: Enigma’s Multi-Source Approach

Rather than relying solely on corporate filings, Enigma aggregates alternative signals that prove business activity. The approach is straightforward: if a business is real, it leaves traces everywhere—just not in traditional corporate databases. Here’s how:

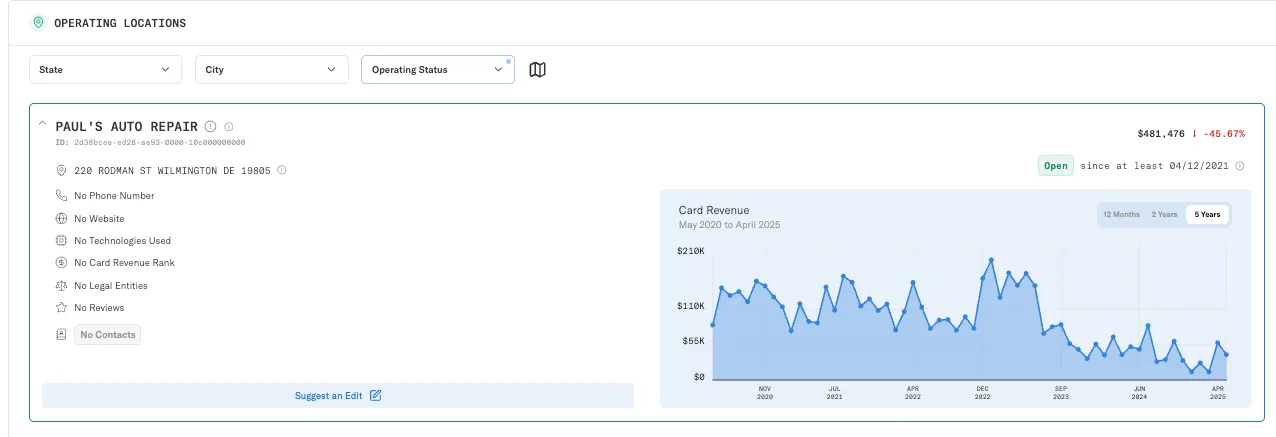

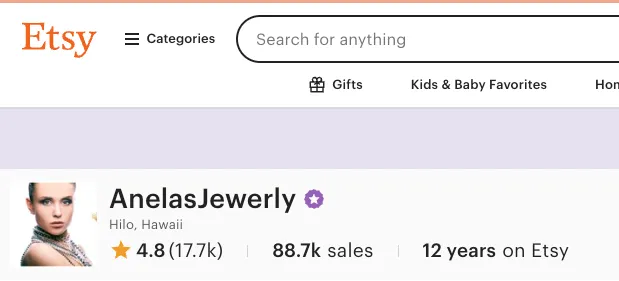

- Online Presence – Many sole proprietors market themselves through social media or personal websites. For example, Paul’s Auto Repair maintains an active presence at Facebook company page, and Anelas Jewelry operates via Etsy, showcasing its products and customer interactions.

- Industry Directories & Review Listings – Some businesses appear in local or industry-specific directories even if they’re not formally registered. Paul’s Auto Repair in Wilmington, DE, operates as a Tire Dealer & Repair Shop and is included in review listings (>80 reviews) despite lacking corporate registration. On the other hand, Anelas Jewelry is a well established business in Etsy. Both businesses would be rejected in traditional KYB checks.

- Key Individuals & Ownership Data – Enigma can provide business ownership, ensuring legitimacy even when corporate registration is absent. Enigma verifies a sole proprietor’s SSN directly with the IRS to verify the business owner is real.

- Revenue Insights – Estimated revenue and transaction data offer additional confirmation of business activity. Pauls Auto Repair in Delaware generates an estimated $<500k card revenues annually, while Anelas Jewelry brings in around $<242k. These types of signals provide clear indicators that consumers have a track record of purchasing from a business over many years as seen with Enigma data.

Paul’s Auto Repair has processed more than $500,000 USD in payment card transactions each year over the past 5 years, but has no corporate registration.

Traditional KYB would have rejected both these established businesses—walking away from nearly $750,000 in combined annual transaction volume from just two merchants. This is why leading verification platforms integrate Enigma into their KYB workflows. When orchestrated through platforms like Alloy, Enigma becomes the critical first step that catches the sole proprietorships other providers miss—all while maintaining the speed and controls that modern platforms demand.

AnelasJewelry has a 12-year track record on Etsy with over 88,000 sales to customers, all operating as a sole proprietor.

Enigma continues to source and incorporate more public data, such as DBA business filings at the local and county level, to expand its business verification data ecosystem. The industry is taking notice—companies like Middesk are also exploring approaches to the sole prop challenge. But the solution requires more than recognition; it demands access to alternative data sources that can reliably verify business activity without traditional corporate filings.

Helping Companies See the Full Picture

For businesses that rely on accurate verification—whether for risk assessment, lending, or marketing—having access to a broader dataset is crucial. Enigma bridges the gap by surfacing sole proprietorships that aren’t captured in traditional records, enabling smarter business decisions and reducing risk.

Sole proprietorships are strange beasts: legally valid, economically important, but structurally difficult to verify. They don’t fit neatly into the frameworks we’ve built for corporate due diligence, but that doesn’t mean they’re inherently high-risk.

It just means we need smarter systems.

The path forward isn’t magic, it’s multi-source, real-world verification, layered together to form a coherent picture. When you start asking “Can I prove this business is real, active, and trustworthy?” instead of “Does it have Articles of Incorporation?” you begin to see through the noise.

In an age of rapidly evolving fraud, powered by AI, that clarity matters more than ever. The sole proprietorship challenge isn’t going away. If anything, the gig economy and rise of solopreneurship mean these businesses will only become more prevalent. Risk and compliance teams can’t afford to wait for traditional KYB to catch up.

For teams evaluating their verification stack today, the question isn’t whether to verify sole proprietorships—regulators have already answered that. The question is whether your current approach can see what Enigma sees: real businesses generating real revenue, just without the corporate paperwork.