The Hidden Economics of Campus Life, Part 1

What $8 Billion in College Spending Reveals

Step onto any American college campus and you’ll encounter a carefully orchestrated economy, one that extracts extraordinary levels of spending from its captive audience of students, staff, and faculty. It’s a marketplace where a single textbook can cost more than a week’s groceries, where parking spaces command luxury hotel prices, and where Sunday laundromats hum with the collective procrastination of thousands. But beyond these familiar college tropes lies a deeper story—one of corporate consolidation, digital disruption, and the surprising resilience of certain business models that have learned to surf the predictable waves of the academic calendar.

We analyzed transaction data from over 70,000 businesses operating within the geographic boundaries of American college and university campuses, tracking billions of dollars in spending across thousands of institutions. What emerged wasn’t just a portrait of campus consumption habits, but a revealing look at how traditional institutions are crumbling while new economic patterns take their place.

The Great Bookstore Collapse

Campus bookstores have been bleeding revenue for years, but the pandemic accelerated what was already a terminal decline. The numbers are stark: bookstore revenue has fallen about 60% from its peak, with 2024 revenues remaining 25% below pre-pandemic levels despite students returning to campus. The median campus bookstore saw revenue decline by 52% in 2020 alone—and most have never recovered.

August remains the one bright spot, still generating about 15% of annual bookstore revenue as families load up on textbooks and college-branded merchandise. But even this back-to-school surge can’t mask the fundamental problem: students just don’t need campus bookstores the way they once did. Along with declining revenue, average transaction sizes have increased from $75 in 2017 to over $95 in 2024, suggesting that students use the campus bookstore only for the most essential purchases, like required course materials that can’t be found elsewhere.

The data reveals three critical patterns. First, the COVID pandemic wasn’t a temporary disruption but an acceleration of existing trends. When campuses closed in March 2020, bookstore revenues didn’t just dip—they cratered, falling by more than 60% at many institutions. Second, the Amazon effect is real and measurable. While some bookstores report 20% or more of revenue coming from online sales, they’re not capturing the shift to digital. Students buy from Amazon, Chegg, or directly from publishers, habits that solidified during the pandemic and show no signs of reversing.

Third, and perhaps most telling, is the extreme seasonality that reveals bookstores’ vulnerability. The typical campus bookstore sees 5-10x revenue swings between peak and trough months. Some campuses experience 15x or greater seasonal variation—a feast-or-famine cycle that makes sustainable operations nearly impossible. When your entire business model depends on a few weeks in August and January, you’re not running a retail operation, but a seasonal pop-up that happens to stay open year-round.

Commercial retailers once thought they could fill the campus bookstore gap. One of the last remaining national brick-and-mortar book retailers operates more than 300 campus locations, all intended to bring efficiency and scale to this struggling sector. Yet our data shows these chain-operated campus bookstores declining just as fast as independents, down 35% from 2017 to 2024. The chain stores do generate 2-3x more revenue than independent bookstores on average, but they’re getting pulled down the same whirlpool. The corporate consolidation that was supposed to save campus bookstores has only managed their decline more efficiently.

Small rural campuses with limited off-campus alternatives maintain some bookstore vitality, while urban campuses with multiple retail options have seen bookstores essentially disappear as economic agents. It’s a bifurcated future for the campus bookstore: monopoly or obsolescence, with little middle ground.

Campus Dining and its Captive Market

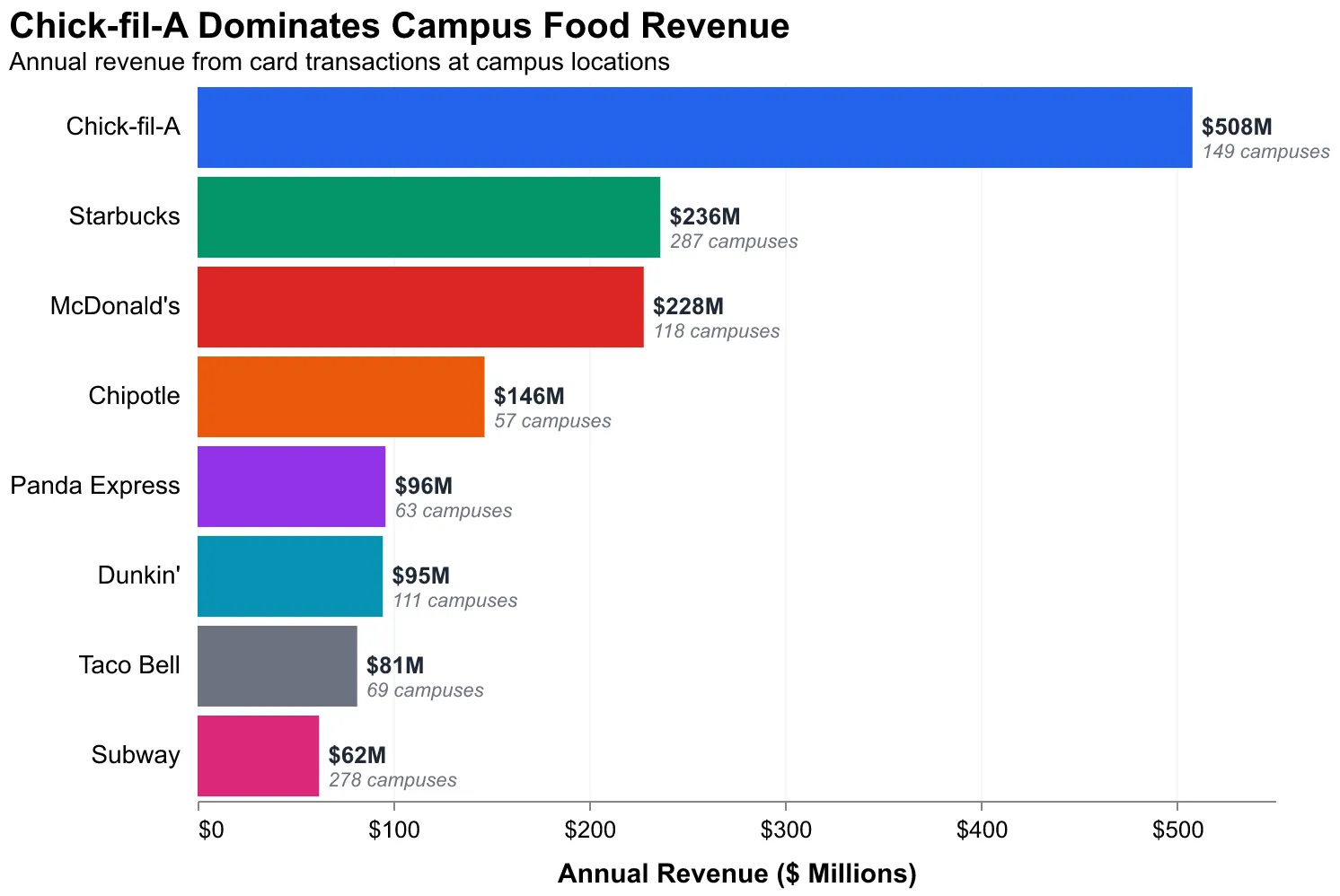

While bookstores collapse, corporate restaurant chains have a solid foothold in campus life. A handful of brands dominate the landscape: Starbucks operates on 280+ campuses, Subway on nearly as many. Together, the top 20 chain restaurants pull in about $1.45 billion in campus revenue.

The concentration is staggering. Our data shows Chick-fil-A generating over $500 million annually from campus locations alone. McDonald’s, Starbucks, Chipotle, Panda Express, and Dunkin’ each pull in hundreds of millions more. These chains have cornered the student market and mastered the academic calendar, adjusting operations and staffing to match the predictable ebb and flow of student spending.

The data reveals which chains are winning and losing the battle for student dollars. Rising stars like Chick-fil-A and Chipotle show 20%+ annual growth, expanding aggressively to new campuses. Meanwhile, despite still-impressive market shares, traditional fast food giants like McDonald’s and Taco Bell are now losing ground to fast-casual options that better match student preferences for perceived quality and customization.

Regional patterns tell their own story, and competition dynamics reveal corporate strategy in action. In-N-Out burgers have earned customer loyalty in California, just as Whataburger is a local favorite in Texas. Meanwhile, Chick-fil-A dominates campus dining in the South with 50% of the fast food market, operating on 111 campuses with regional revenues of $396 million. On campuses where both Starbucks and Dunkin’ operate, Starbucks wins a narrow 52% of the time nationwide, yet still generates on average 60% more revenue than its Massachusetts-based rival. Still, Dunkin’ holds its ground in the Northeast, where brand loyalty runs deep and preferences were formed long before students arrived on campus. On Massachusetts and New York campuses, Dunkin’ averages 40% higher revenue than the national average.

Summer Survivors and Seasonal Extremes

When students leave for summer, most campus businesses see revenues crater. But some categories show remarkable resilience. Our data reveals which businesses serve the entire campus community versus those that are mostly dependent on the undergraduate population.

Parking maintains 85% of its academic-year revenue during summer months—likely because many staff, faculty, and graduate students still need to park as they work through the slow season. Coffee shops also retain about 70% of their revenue, serving those who work on campus all year round. Convenience stores and pharmacies actually see some of the smallest drops, maintaining 75-80% of regular school year revenue.

But for most other businesses, summer is a wasteland. Bars see revenue drop 70%. Fast food falls 60%. Bookstores essentially hibernate, with some reporting 90% revenue declines in June and July. These seasonal swings create a brutal business environment where nine months of revenue must cover twelve months of costs.

In terms of upswings, the most extreme seasonal patterns also belong to businesses tied directly to the academic calendar. Some campus bookstores see August revenues 20x higher than July. Certain dining establishments report September revenues 15x their summer lows. These aren’t just gradual seasonal patterns, but drastic extremes that require careful cash management and flexible staffing to survive.

What This Means

Our data tells a story of transformation through transactions. The American college campus has always been a strange commercial ecosystem—a place where teenagers with limited budgets somehow sustain billions in annual commerce, where monopolies thrive behind the veil of convenience, and where the academic calendar creates business patterns unlike anywhere else. But this ecosystem is evolving rapidly, shaped by generational changes in shopping behavior, technological disruption, and the increasing corporatization of campus life.

The $8 billion we see flowing through U.S. campus businesses each year isn’t just consumer spending, but rather the physical manifestation of college life itself, measured in coffee cups and late-night pizzas, in overpriced textbooks and parking tickets, in all the small transactions over the course of an expensive education that launches American youths into adulthood.