KYB vs. KYC: Two Different Paths to Trust in Customer Onboarding

Introduction

In today’s financial ecosystem, compliance and trust are non-negotiable. Every transaction, whether made by an individual consumer or a business entity, requires confidence that the counterparty is who they claim to be.

That’s where Know Your Customer (KYC) and Know Your Business (KYB) come in. These two compliance processes are often mentioned together, but they serve different functions. KYC verifies individuals. KYB verifies businesses—which themselves may be corporations, LLCs, partnerships, or even sole proprietors operating under their own names.

Both processes are vital. KYC is the regulatory foundation for consumer-facing businesses, while KYB ensures that organizations can confidently transact with other businesses. Together, they form a comprehensive framework for reducing fraud, managing risk, and staying compliant.

KYC 101: Why Compliance Starts with Individuals

Know Your Customer (KYC) is designed to verify an individual’s identity and assess risk before they are onboarded. It is a key requirement under anti-money laundering (AML) and counter-terrorist financing (CTF) regulations, enforced globally by authorities such as the Financial Action Task Force (FATF), the Bank Secrecy Act (BSA) in the U.S., and the EU’s AML directives.

The goals of KYC are threefold:

- Prevent financial crime — stopping money laundering, terrorism financing, and fraud.

- Ensure regulatory compliance — meeting obligations under AML and CTF laws.

- Build trust in the financial system — ensuring that only legitimate individuals can access services.

Typical KYC Process

KYC generally requires:

- Identity verification: A government-issued ID such as a passport or driver’s license.

- Proof of address: Utility bills or bank statements.

- Watchlist and sanctions screening: Ensuring the individual is not flagged by OFAC, Interpol, or other authorities.

- Biometric verification: Liveness detection and facial recognition are increasingly standard to prevent stolen ID use.

Over the last decade, KYC has become increasingly sophisticated. Providers such as Trulioo, Onfido, Jumio, and Socure have emerged as leaders, leveraging AI and machine learning to verify identities in real time. This innovation has transformed KYC from a manual, paper-heavy process into a near-instant digital experience.

But KYC only covers individuals. Businesses require something deeper.

Why KYB Goes Further: Verifying Businesses

When your customer isn’t just a person but a business, KYC alone isn’t enough. A business is more than just a name—it is often a legal entity with its own registration, tax obligations, ownership structure, and potential risk exposure.

That’s where Know Your Business (KYB) comes in. KYB extends compliance to business entities by verifying not only the company itself but also the individuals behind it, such as beneficial owners and key executives.

The Core KYB Questions

KYB typically asks:

-

Is the business registered and active? Validation through state or national registries.

-

**Does the Taxpayer Identification Number (TIN) match IRS or equivalent tax authority records?

**

-

Who are the ultimate beneficial owners (UBOs)? Identifying key owners and other individuals with significant control.

-

**Does the business or its owners appear on sanctions or adverse media lists?

**

-

Does the industry represent heightened risk? For example, a company may want to know if their customer operates money services, crypto exchanges, gambling, or adult content..

Middesk’s KYB 101 makes clear that this is not a simple matter of checking a single ID. Instead, it’s about piecing together fragmented and often inconsistent data across multiple sources.

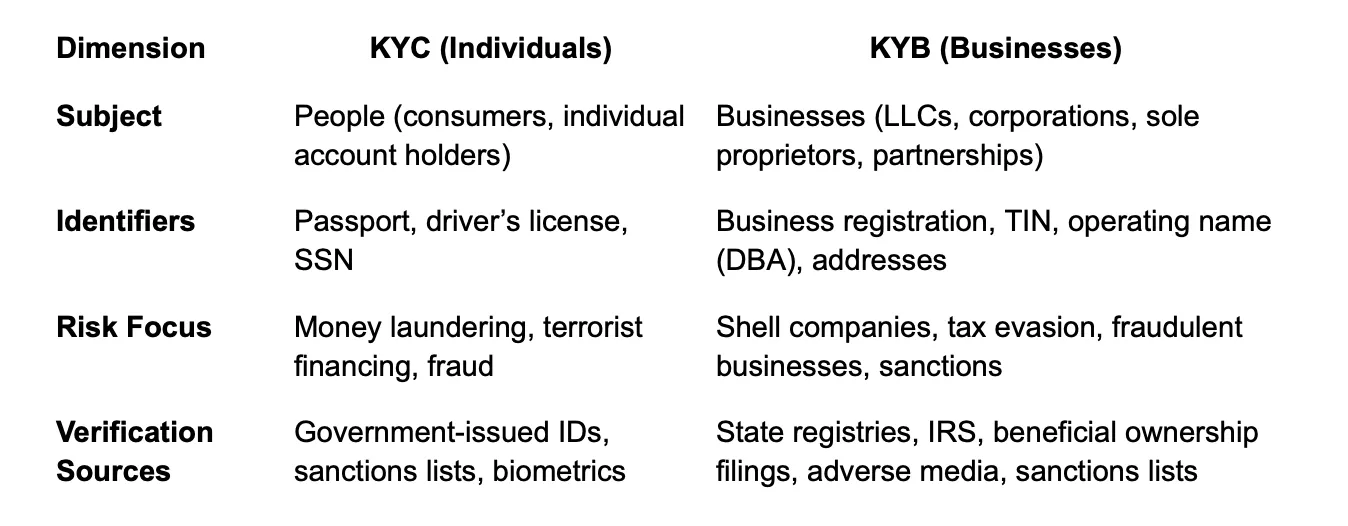

KYC vs. KYB: Two Distinct Compliance Paths

While KYC and KYB are both compliance processes, they differ in important ways:

The key takeaway is that KYB is not “better” or “more advanced” than KYC. Instead, they are different. KYC ensures that individuals are legitimate. KYB ensures that businesses—including those run by individuals—are legitimate. Together, they create a complete compliance foundation.

Why KYB is Particularly Hard in the U.S.

Unlike KYC, where most countries have centralized identity documents, KYB in the U.S. faces unique structural challenges:

- Decentralized Registries: In the U.S., legal entities are created and governed by each state separately. Each state maintains its own corporate records with no nationwide equivalent. Access, quality, and update frequency vary widely.

- Multiple Naming Conventions: Businesses can operate under legal names, DBAs (doing business as), and brand names. Matching across them is non-trivial.

- Ownership Transparency Gaps: Until very recently, beneficial ownership information was limited and inconsistent. The Corporate Transparency Act (CTA) aimed to improve this, but implementation is controversial and ongoing.

- High Volume of Small Businesses: The U.S. has over 33 million small businesses, and private businesses in the U.S. generally do not publish sophisticated or standardized public filings.

These challenges make business verification slower, costlier, and riskier compared to consumer onboarding.

The Enigma Difference in KYB

Traditional KYB providers rely on black-box risk scores, designed to be interpreted by analysts in manual workflows. Enigma takes a more transparent and automated approach:

-

**Granular, Ground-Truth Data

**Instead of abstract scores, Enigma surfaces the raw facts: corporate registrations, TIN validation, ownership, addresses, and watchlist status.

-

**Speed and Automation

**Enigma’s KYB API delivers verification in under three seconds by resolving fragmented records into confident matches.

-

**Transparency and Explainability

**Every output is paired with reasoning (e.g., “address exact match with Secretary of State filing”) so compliance teams can understand and trust the result.

-

**Coverage Beyond Corporations

**Enigma verifies not only corporations and LLCs but also sole proprietors, partnerships, and small businesses—segments often underserved by legacy providers. Enigma, unlike other traditional KYB providers, can verify real sole props and microbusinesses in the US through trusted sources beyond Secretary of State records.

This approach helps reduce onboarding friction while meeting stringent compliance standards.

KYC and KYB Together: The Full Picture

Crucially, KYC and KYB often overlap. A business entity might pass KYB checks, but regulators also require person-level verification of its beneficial owners. In practice:

- Sole Proprietors → Require both personal KYC and business KYB.

- SMBs and Corporations → Require KYB on the entity + KYC on executives/owners.

This layered approach ensures both the business and the people behind it are legitimate.

The combination is essential in preventing common risks:

- Fake businesses used as fronts for money laundering.

- Legitimate businesses controlled by sanctioned or high-risk individuals.

- Individuals misrepresenting themselves as businesses to bypass fraud controls.

By integrating KYC and KYB together, financial platforms build a holistic defense against fraud and non-compliance.

Achieving best-in-class KYB coverage while reducing EDD Manual reviews

The Enigma KYB API integrates with orchestration platforms like Alloy and Taktile, helping clients such as Wisetack and Chase build cost-efficient, multi-vendor compliance workflows. One payment processor cut per-call costs by 60% by using Enigma first for Secretary of State (SoS) matches, while improving approval rates with trusted sources beyond SoS filings.

Yet even with strong KYC + KYB strategies, manual reviews for Enhanced Due Diligence (EDD) remain inevitable. Compliance analysts often spend 10–30 minutes per case resolving aliases, validating ownership, or digging through fragmented government records. Enigma’s Model Context Protocol (MCP) changes that.

Enigma MCP anchors reviews in a ground-truth business identity graph built from billions of federal, state, and municipal filings. It pre-resolves variations (e.g., DBAs vs. legal names), surfaces ownership hierarchies, and provides structured, source-attributed summaries. This reduces research time to minutes—or even seconds—while increasing confidence in match accuracy.

Some clients are now layering programmatic agents on top of MCP, automating straightforward reviews and escalating only complex exceptions, enabling compliance teams to scale without sacrificing rigor.

Conclusion

KYC and KYB serve different but complementary roles in compliance. KYC ensures that individuals are legitimate; KYB ensures that businesses are legitimate. Both are critical for reducing fraud, managing risk, and meeting regulatory requirements.

While KYC is now a relatively mature and standardized process, KYB remains fragmented and challenging—especially in the U.S., where state registries and ownership data are inconsistent. That’s why KYB solutions require not just data, but intelligent resolution, automation, and transparency.

Enigma is building the KYB infrastructure to meet this challenge. With instant verification, granular data, and explainable results, we help platforms onboard more good businesses faster—while maintaining the highest standards of compliance.

In a digital-first world, the winners will be those who can seamlessly verify both people and businesses. At Enigma, we’re making that possible.