A Guide to Card Transaction Data

Data about debit and credit card transactions can be a powerful tool for understanding consumer spending trends.

Eight in 10 Americans report they have at least one credit card, and there were more than 511 million active consumer credit cards in the United States in Q1 2020.

The pandemic accelerated movement away from cash: according to McKinsey, by the end of 2020, U.S. consumers used cash for just 28% of transactions, compared to 51% a decade prior.

What is card transaction data?

“Card transaction data” typically refers to data generated when a credit card is used to purchase goods and services from a business. To protect privacy, individual card holders are anonymized and transactions are aggregated.

But card transaction data can include more than just consumer credit cards. The card data can be derived from all kinds of cards, including debit cards, small business cards, corporate cards, and charge cards. The data can also include digital transactions, also known as “card not present” transactions.

Where does card transaction data come from?

Transaction data provided by data companies can come from a variety of sources. Data may come from a bank integration. Data can also be aggregated by a card issuer, a credit card network, or a payment processor at the point of sale.

When working with transaction data, it’s crucial to understand what kind of source it comes from. Many sources may skew towards certain groups of consumers, geographic areas, or types of transactions. Knowing the size of the sample and any biases in the data source enables you to better understand how to derive trustworthy insights from the data.

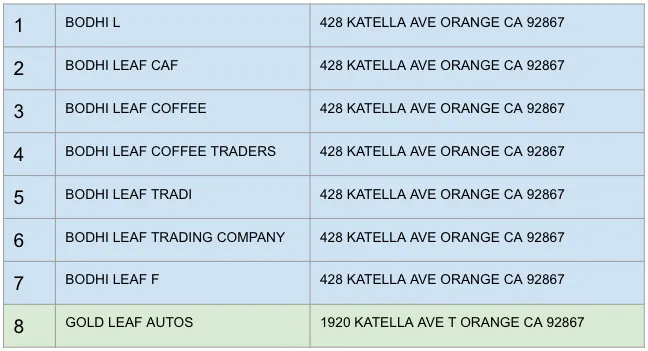

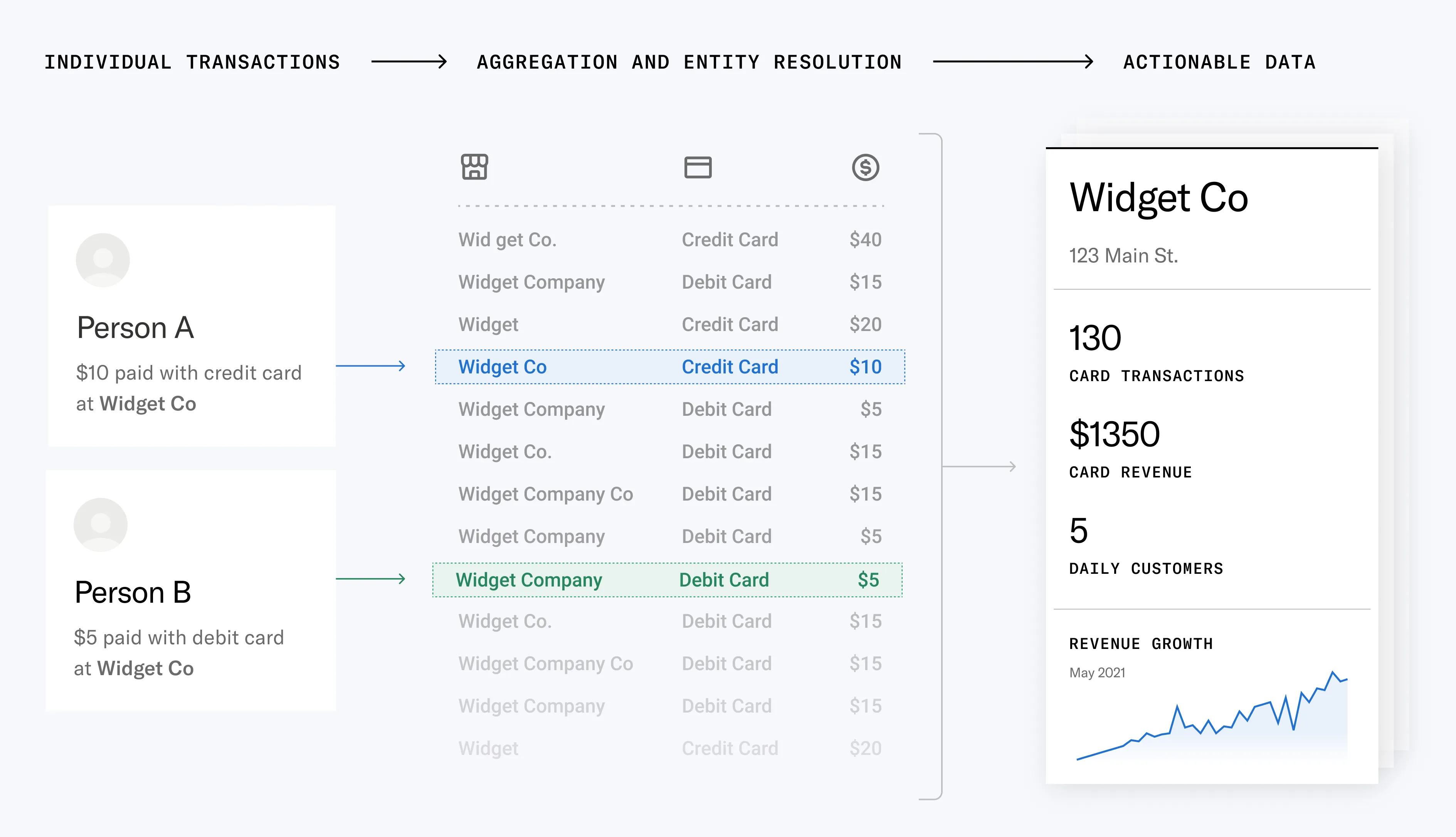

Raw transaction data is notoriously difficult to analyze. The challenge: in its raw form, the data is messy, inconsistent, and sometimes duplicative, requiring organization and cleanup at scale before it’s ready to tap for insights.

Here’s an example. Below, looking at raw transaction data, in blue, for the Bodhi Leaf coffee shop in Orange, California, we see that different payment processors refer to the same business as “Bodhi L,” “Bodhi Leaf Coffee,” “Bodhi Leaf Coffee Traders,” “Bodhi Leaf Trading Company,” and “Bodhi Leaf Tradi.”

Uniting this data into a holistic view of transactions at a business level requires sophisticated algorithms and entity resolution techniques to clean and match the data.

How you can use card transaction data as an indicator of business performance

Historically, card transaction data analytics has been used as a bellwether for consumer trends. When aggregated at the cardholder level, this data helps both marketers and government agencies understand buyer preferences and macro economic trends.

Recently, however, it’s been recognized that card spending data can also provide valuable insights about the health of a business. Looking at trends in card revenues, transaction volumes, and customer concentrations can reveal whether a business is growing or declining. When aggregated by business, this data is often referred to as “merchant transaction data.”

Card revenue does not reflect all of a business’s revenue, but COVID-19 has accelerated the trend of consumers using cards over cash. Merchant transaction data is especially helpful for businesses operating in industries where a high proportion of transactions are made by card, for example retail shops, restaurants, and service providers.

Merchant transaction data can help multiple teams at an organization:

- Underwriting teams incorporate card revenue and transaction trends into their models for more accurate setting of initial credit limits.

- Risk teams use fresh monthly revenue data to monitor the health of their customer portfolios and mitigate potential damage before it occurs.

- Marketing teams use revenue and transaction data to improve lead segmentation and scoring, as well as purge their lead databases of closed businesses to improve campaign ROI.

- Sales teams use revenue trends to identify fast-growing businesses and prioritize their prospecting targets.

What to consider when selecting a transaction data source

When evaluating a card transaction dataset, asking the right questions can help you compare the options and understand which dataset best suits your needs.

What is the latency?

- How fresh is the data? How frequently is it updated?

What is the coverage?

- How many cards are included in the panel? Is it just credit cards or debit cards as well? How many businesses are covered in the dataset?

What is the bias of the credit card panel?

- What is the scope of the panel? Is it just Visa or just Mastercard? Is it skewed to certain geographies or income classes?

How can I use it?

- Some data providers may require you to get permission from a business before accessing its transaction trends. Others, like Enigma, have already integrated privacy protection into their system so that you can immediately access data about any business.

Interested in learning more about Enigma’s Merchant Transaction Signals? Get in touch for a demo.